AARP Hearing Center

Medicare doesn’t automatically cover prescriptions, but you can buy Part D drug coverage from a private insurer. The costs you may pay out of pocket include:

- A premium, your plan’s monthly bill.

- A copayment, a set fee based on the plan’s rules that you pay to a pharmacy for each of your prescriptions after you meet any deductible.

- A deductible, the set amount you pay to a pharmacy each year before the insurance kicks in.

- Coinsurance, the percentage of costs you pay to a pharmacy for each of your prescriptions after you meet any deductible.

You can purchase either a stand-alone Part D plan or get health and drug coverage through a Medicare Advantage plan. You can acquire this coverage when you first enroll in Medicare or during open enrollment, Oct. 15 to Dec. 7 each year for coverage starting Jan. 1.

You also may be eligible to buy coverage or switch plans at other times. The average Medicare beneficiary has a choice of 59 Medicare plans with Part D drug coverage in 2024, including 21 stand-alone Part D plans and 36 Medicare Advantage plans with drug coverage, according to KFF, formerly the Kaiser Family Foundation.

Private companies that sell Medicare Part D coverage set their own premiums, deductibles and copayments but need to follow the federal government’s rules. For example, Part D plans can decide to charge a deductible, but the maximum deductible can’t be more than $545 in 2024.

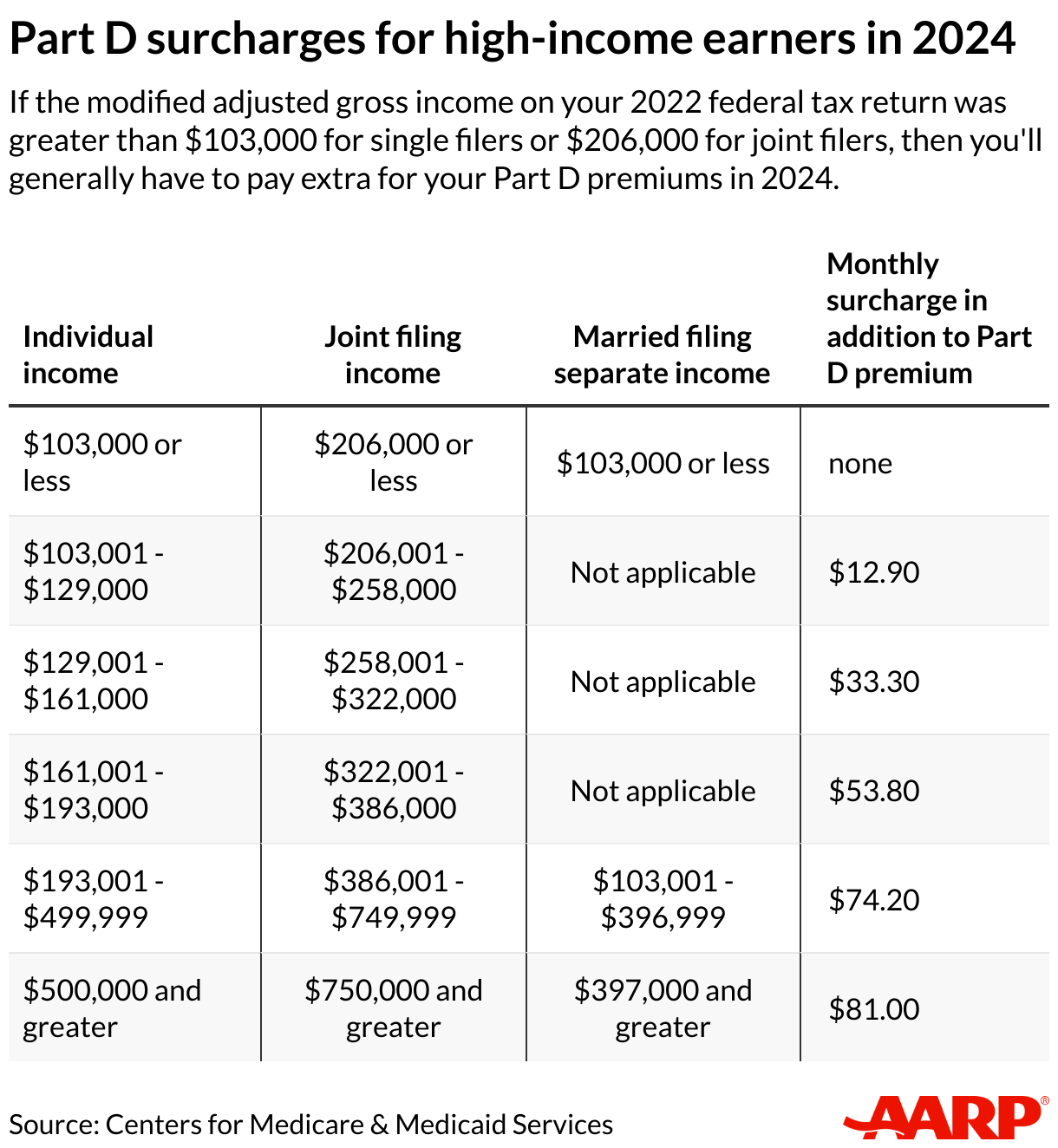

Your actual costs for Part D depend on the options in your area, the plan you select, how much it charges for your medications, how much you’ve paid for drug costs so far during the year and your income.

How much are Part D premiums?

The average premium for a stand-alone Part D plan is $55.50 a month in 2024. But the specifics can vary a lot by plan.

Average monthly premiums for stand-alone Part D plans range from less than $1 to nearly $200 per month in 2024, according to KFF. The full range of premiums may not be available in your area.

If you choose a Medicare Advantage plan with drug coverage, you’ll generally pay one monthly premium for all benefits — hospital, medical and prescription drugs. The average monthly premium for Medicare Advantage enrollees is $18.50 in 2024 in addition to the standard Part B premium of $174.70.

If you didn't sign up for a stand-alone Part D policy or a Medicare Advantage plan with drug coverage when you were first eligible and you don't have similar drug coverage from another source, such as a retiree plan or Tricare military health care, then you may have to pay a permanent late enrollment penalty for Part D.

Next in Series

Can I Get Help Paying for My Prescriptions?

Federal program can help with costs if your income is low