MONEY SAVER

How I Saved $4,400 in a Day … and (Maybe) You Can Too

Some simple negotiation tricks and a little time can go a long way toward keeping cash in your pocket

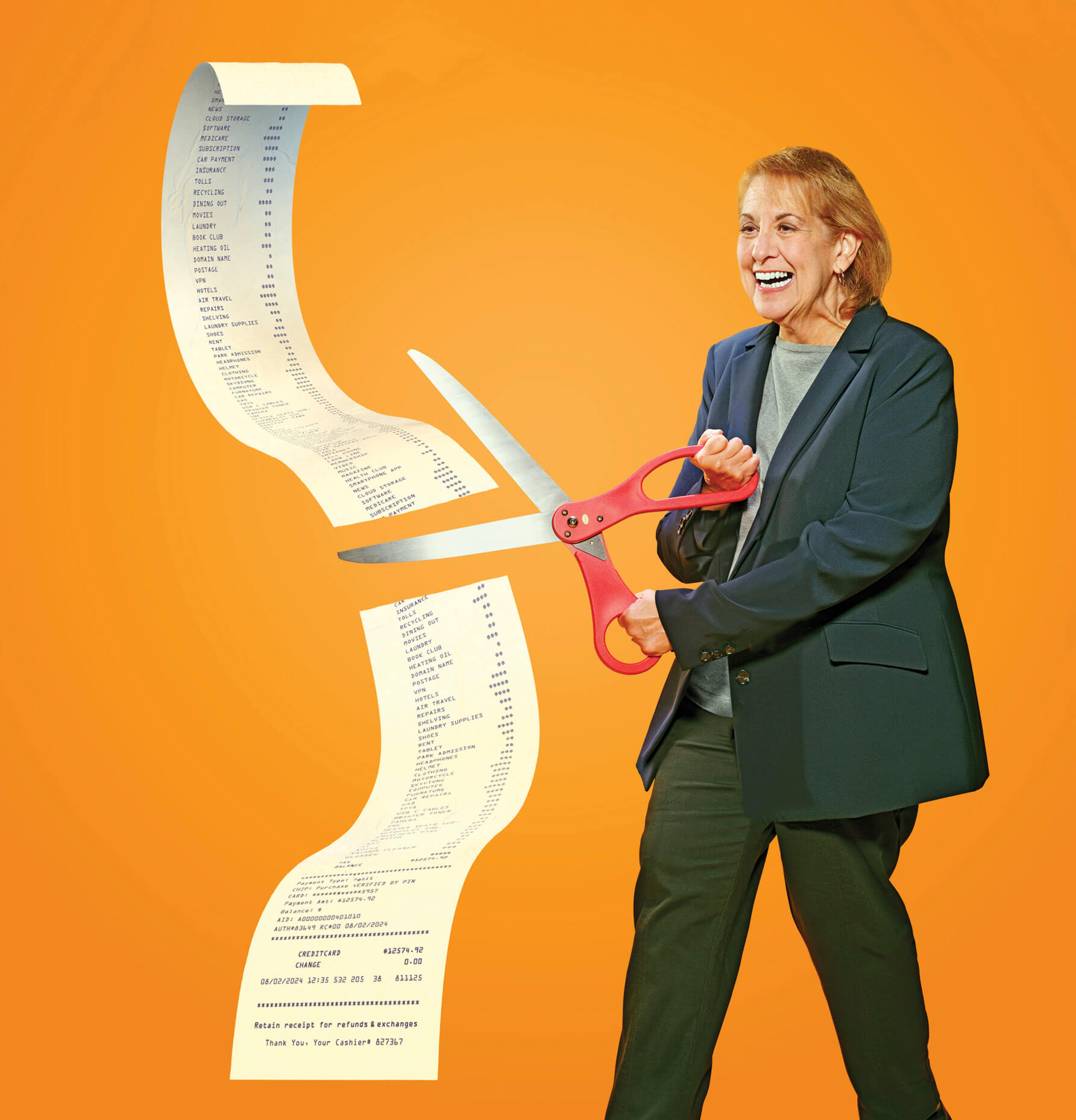

HOW MUCH money could you save if you spent one full day trying? I recently decided to find out, tackling as many money-saving tasks as I could in a nine-to-five workday—all the pesky stuff I kept meaning to do but never made time for.

The result for me: eye-popping savings, on an annualized basis, of precisely $4,466.41.

Along the way, I learned some seriously valuable lessons. For one, it’s easy to get a deal on almost everything; the real challenge is how big a price cut you can nab. Also, there’s a simple formula to achieve the biggest savings. Finally, the benefits of this exercise go far beyond dollars and cents.

Here’s what I did—and how you can do it too.

Go for the easy wins first.

I spent the first hour of the day identifying my recurring bills and determining which ones to cut or renegotiate. This step revealed two streaming services I’d forgotten I had, a handful of subscriptions to magazines I rarely read and a mystery monthly charge from Apple. All told, I was spending about $100 more a month on these services than I’d guessed.

I’m hardly alone. Consumers, on average, estimate they spend $86 a month on subscription services, while their actual outlay is $219 a month, reports C+R Research.

Armed with my checklist, I started with the most straightforward task: canceling subscriptions. A pattern became apparent: I’d click to cancel, then get a reminder of how great the service was; click to cancel again, then get an offer with modest savings; click to cancel a third time and get a much better deal.

“The company’s goal is to get you to stay on as a customer while giving away as little as possible, so they will never offer their best deal first,” says Yahya Mokhtarzada, cofounder of Rocket Money, a budgeting app that helps track and cancel recurring charges.

Although this was a useful strategy to learn—hold out as long as possible!—I ignored the enticements and clicked goodbye in quick succession to five magazines and the forgotten streaming services. Then, scrolling through my phone, I figured out that the mystery Apple charge was for an app I no longer use. So I dropped that too.

Time spent: 2 hours, 10 minutes

Savings: $1,078.53 per year

Deal with a human.

To get the best offers, pros had told me, you must talk to a person. So for services I wanted to keep, I hit the phone.

I followed this basic script: “Say you want to cancel your service. That will get you to the retention department, where they have more liberty than a regular customer service rep to give you as much as you can squeeze out of them,” says Barry Gross, president of BillCutterz, a subscription-negotiating service. “Keep your questions open-ended, like, ‘What can you do to help me reduce my bill?’ and keep asking, ‘What else can you do for me?’ ”

First up was my $498.88-a-year Wall Street Journal digital subscription. The rep quickly offered what seemed like a sweet deal: a three-year plan for $99 for the first year, then $299 and $467 for subsequent years. I took it. That was a rookie mistake. If I had checked the WSJ website, I would have seen a new-customer offer for $52 a year. Knowing that, I could have asked for the same price.

Resolving to do better, I checked the New York Times website before calling them. So when a rep offered to reduce my $51-a-month charge for digital access and the Sunday print edition to $25.52 a month for six months, I mentioned a new-customer promotion I’d seen: $20 a month for a year. The rep countered with $12.40 a month for six months, then $24.80 for the following six months. Score!

Time spent: 40 minutes

Savings: $788.68

Save the thorniest bills for last.

Getting a price cut on cellphone service is tough, typically. “They keep you on the phone for a long time to wear you down and overload you with confusing details about different plan options that often don’t offer any real savings,” says Mokhtarzada.

That matched my experience with Brenda, a cheery Verizon agent who said she’d be happy to help lower my bill. She offered me—“don’t laugh,” she said—$4 off my $234-a-month family plan as a reward for my 20 years as a loyal Verizon customer.

I laughed anyway. “What else can you do for me, Brenda?” I asked.

She then bombarded me with features of plans I could switch to, none of which would cut my bill more than a dollar or so. “I don’t need those features,” I said. “I just want to save money.” This went on for an hour until an exasperated Brenda asked, “How much do you need to save?” At least $50 a month, I said. Then she magically found a new basic plan, which, along with dropping a hot spot on two lines and insurance on another, cut my monthly bill by $51.

Later I learned I’d made another rookie mistake. “Typically you can get the discount without giving up anything in terms of service,” says Mokhtarzada.

The last item on my agenda took the most time but yielded the biggest savings: applying to have my Medicare premiums adjusted due to a “life-changing event.” For me, that event was my recent move from a staff job as deputy editor of Newsweek to freelance writing and editing work that pays far less. Since my Medicare premiums are based on the income reported on my tax return from two years ago, my husband and I are paying $1,987.20 per year more than we should pay, based on my current income. So I filled out an application for the adjustment, then uploaded it with the necessary documentation.

Time spent: 3 hours, 37 minutes

Savings: $2,599.20

Keep the momentum going.

The most delightful part of my day wasn’t how much cash I put in my pocket. It was how exhilarated I felt and motivated I was to keep the game going. On my next money-saving day, I’ll tackle my cable and internet bundle and my homeowners insurance.

“There’s very little downside to trying; at worst, you’ll break even,” says Lending Tree’s Matt Schulz, author of Ask Questions, Save Money, Make More. At best, like me, your savings may run into the thousands. Not bad for a day’s work.

Longtime journalist Diane Harris was formerly the top editor of Money magazine and deputy editor of Newsweek.