This Is 50

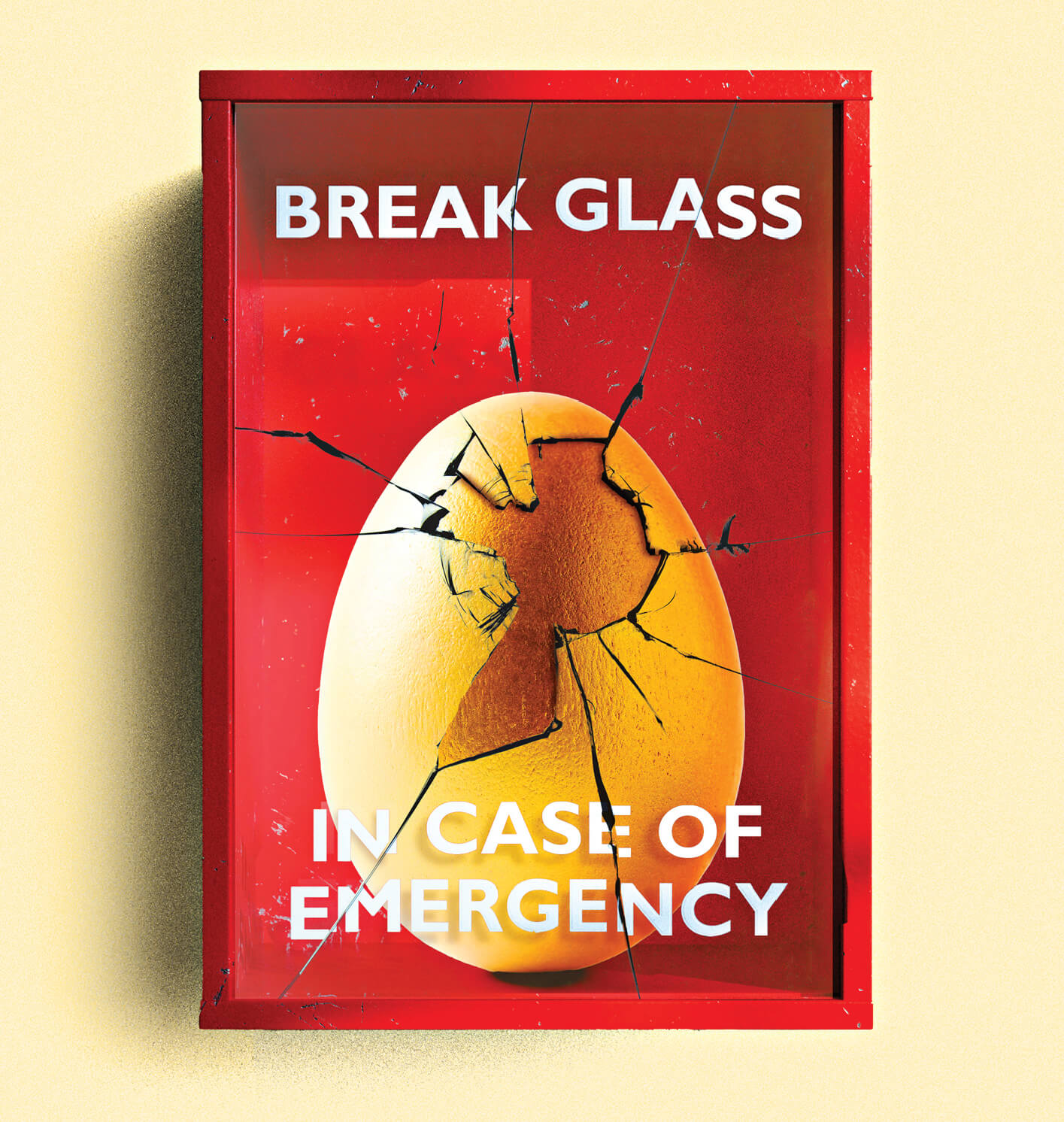

Emergency Cash From Your 401(k)

New rules let you withdraw $1,000 without penalty—but should you?

FINANCIAL EXPERTS advise keeping three to six months’ worth of living expenses in an emergency fund—but that’s not always easy to do. In fact, 76 percent of Gen Xers have less than six months’ emergency cash, including 31 percent who have none at all, according to a recent Bankrate report.

So, what to do in a financial crisis? New rules make it easier to dip into your retirement account without penalty. But there are some pretty significant caveats.

Typically, when you take money from an IRA or 401(k) before age 59½, you pay a 10 percent penalty on top of income taxes on the money. But a new IRS rule lets retirement plan owners withdraw up to $1,000 for personal or family emergency expenses, penalty-free.

What constitutes an emergency? The IRS leaves that up to you, but examples include medical care, auto repairs and imminent foreclosure, and you may have to give your plan administrator your word, in writing, that the financial need is real.

In tough times, the new rule can be a powerful tool, says Barbara Rayll, vice president of product and solutions management for Texas-based Corebridge Financial. But there are drawbacks. “Spending out of your retirement plan not only reduces the amount you have saved but also your earning power,” since the money won’t be earning market returns, interest or dividends, she notes.

You can take only one distribution in a calendar year, and after you take one, you can’t take another for three years—unless you pay the first one back. These limits are designed to make you pause before raiding your 401(k). And that’s a good thing, Rayll adds: “You should always think twice before touching your nest egg, particularly as you approach retirement age.” —Tamara E. Holmes

MY FIRST

KNEE PAIN

IN ALL MY YEARS of sports, I had never had knee issues. Ankle sprains, many. Muscle strains, yep. But my knees were always reliable, until I reached my later 50s, and one morning, I felt a twinge during a jog with a friend.

Out of caution, I swore off running for two weeks but dove into painting my son’s bedroom instead. Within a day, my right knee had ballooned with fluid.

“Bursitis,” my doctor said. He put me in a knee brace for 10 days. My inner 30-year-old was appalled.

Once the brace was off, I fell into a disjointed pattern of walking, hiking, jogging, biking and inactivity, guided by my knee’s response. The lack of predictability put me off-kilter.

When I finally visited a sports medicine clinic, the specialist diagnosed osteoarthritis. “If you ever had bursitis, you don’t anymore,” he told me. He prescribed physical therapy and a nonsteroidal anti-inflammatory gel.

The physical therapist assigned exercises. Three to four times a week, I cycle through stair “step-downs,” standing clamshells, leg squats and lunges, heel raises, side planks with one leg raised, and forward “T” one-legged balancing.

The exercises have helped some: I can usually hike when I want to now. But my knee never feels totally normal. Still, PT has big perks. My ankles are stronger, my core strength has increased, and my lower back feels the best it has in years. These are exercises I’ll be doing for life.

The jury’s still out on how much I’ll be running in the future, but meanwhile my balance is bombproof. It isn’t what I wanted, but it’s not nothing. I can hear my inner 80-year-old cheering me on. —Joanna Nesbit

MEMBER CHECK LIST

EXTEND YOUR MEMBERSHIP NOW AND SAVE

To continue providing the high-quality information and benefits you enjoy, AARP dues will increase in 2025. This is the first increase in 15 years. Extend your membership at current pricing today. Visit aarp.org/lockinsavings or use your phone to scan this code.